Private Equity CEO Predicts AI Will Reshape Deals

When a private equity CEO predicts AI will change the business, the useful question is which parts, and on what timeline.

Blake Aber · Predicate Ventures

The prediction, stated plainly

A private equity CEO predicts AI will move from a marketing line into the core of how firms operate. The claim is not that software replaces investors. It is that the work of sourcing, diligence, and portfolio management gets faster and cheaper per unit of output.

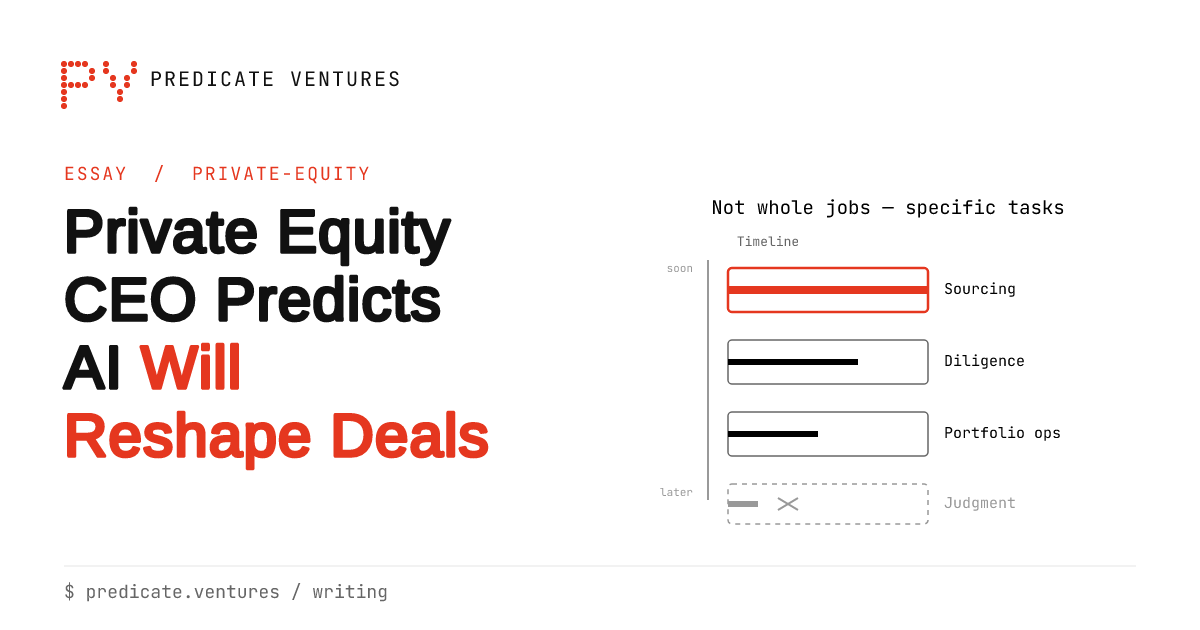

That framing matters. Predictions about AI often collapse into two camps: everything changes, or nothing does. The more grounded view sits between them, and it maps to specific tasks rather than whole job functions.

Where the change lands first

The earliest effects show up in tasks that are repetitive, text-heavy, and already well-documented. Private equity has plenty of these.

Deal screening is one. Firms review far more targets than they buy, and most of the early filtering is reading. Financial summaries, market notes, and management materials all pass through analysts before anyone commits real time. Models that read and rank these documents shorten the first pass.

Diligence is another. Contract review, customer concentration checks, and comparison against precedent deals are structured enough for machines to draft first and humans to verify. The output is a starting document, not a final call.

What stays human

Judgment about people, incentives, and timing does not automate well. Whether a management team executes under pressure, whether a market holds, whether a price reflects real risk. These decisions rest on reading situations that resist clean data.

The prediction assumes AI handles the reading and drafting while partners keep the decisions. That division holds only if firms treat model output as a draft to challenge, not an answer to accept.

Portfolio operations, not just deal-making

The more durable claim concerns portfolio companies after the deal closes. This is where a private equity CEO predicts AI will produce measurable returns.

Many portfolio companies run functions that AI touches directly. Customer support, sales operations, finance close cycles, and marketing content all carry labor cost that models reduce. A firm that owns dozens of companies can apply the same playbook across all of them.

That repetition is the point. A single company adopting AI captures a local gain. A private equity firm rolling the same approach across a portfolio captures the gain many times, and it can measure results across a controlled set of businesses.

The margin math

Private equity returns depend on buying a business, improving its operations, and selling at a higher multiple or higher earnings. AI enters on the operations side by lowering cost or raising output without proportional hiring.

If a portfolio company cuts service cost while holding quality, margin improves. Improved margin supports a higher exit price. The prediction reduces to a claim that AI adoption becomes a standard lever in the operational improvement toolkit, sitting alongside pricing changes and procurement.

The risk in the prediction

Every adoption story carries a cost story, and this one has three.

The first is measurement. Firms that count AI savings before checking quality tend to reverse course. A support system that closes tickets faster but leaves customers unhappy trades a visible metric for an invisible loss. Honest measurement requires tracking outcomes the model does not optimize for.

The second is integration cost. Dropping a model into an existing workflow rarely works on the first attempt. Data has to be cleaned, staff has to be trained, and processes have to be rebuilt around the new tool. The savings arrive after the investment, not before.

The third is uniformity risk. When many firms apply similar AI playbooks, the operational advantage narrows. If every buyer can raise margins the same way, the improvement gets priced into acquisition multiples, and the excess return fades. Early movers gain; the field catches up.

Reading a CEO's prediction critically

When a private equity CEO predicts AI will drive returns, the statement serves two audiences at once. Limited partners hear a firm that stays current. Portfolio managers hear a directive to adopt.

Both readings are reasonable, and both can be true while the specifics stay vague. The useful test is whether the prediction attaches to measurable claims: which functions, what cost reduction, over what period, verified how.

Predictions without those attachments are positioning. Predictions with them are operating plans. The distinction tells you whether a firm has done the work or is describing an intention.

Questions worth asking

An investor or operator evaluating such a prediction can push on a few points.

Which portfolio companies have adopted AI, and what did results look like against a baseline. How does the firm separate AI-driven gains from other operational changes. What did integration cost, and how long until payback. What quality metrics guard against savings that hide losses.

Answers to these reveal whether the prediction rests on evidence or enthusiasm.

What this means for the sector

The direction of the prediction is likely correct. AI reduces the cost of document-heavy and repetitive work, and private equity contains a lot of both. Adoption spreads because the economics favor it.

The timeline and magnitude are the open questions. Task-level gains arrive quickly and are easy to demonstrate. Portfolio-wide, verified return improvement takes longer and depends on execution that varies widely between firms.

The firms that gain most will treat AI as an operational discipline with measurement attached, not a theme to announce. They will track quality alongside cost, invest in the unglamorous integration work, and accept that the advantage erodes as competitors adopt the same tools.

A private equity CEO predicts AI will change the business. The prediction holds. What separates the firms that benefit from the ones that merely talk about it is the willingness to measure, and the honesty to report what the numbers actually show.